27 May 2026

Supplier Showcase: Italian Tomato Processing with Steriltom & Italtom

Lupa Foods is thrilled to showcase our partnership with Steriltom and Italtom,...

OVERVIEW

There’s been an increase in the cost of raw material compared to historical prices. However, this season a large portion of the overall cost is being driven by increases outside of raw material costs.

Energy has become the key driver of increased costs as opposed to the raw material itself. In 2022, as with many other products and ingredients, it’s vital to look past the ingredients itself to see why we are experiencing price inflation.

| 3KG TIN | 2021 | 2022 | VARIATION % |

| TINS EURO/TIN | 0,220 | 0,490 | 122,73% |

| LIDS EURO/TIN | 0,065 | 0,100 | 53,85% |

| CARDBOARD EURO/TIN | 0,05 | 0,08 | 78,57% |

| ENERGY EURO/TIN | 0,08 | 0,19 | 140,00% |

| RAW MATERIALS ON AVERAGE | 1,08 | 1,20 | 11,11% |

| TOTAL COST PER TIN | 1,49 | 2,06 | 38,32% |

| EURO/USD | 1,13 | 1,03 | 8,85% |

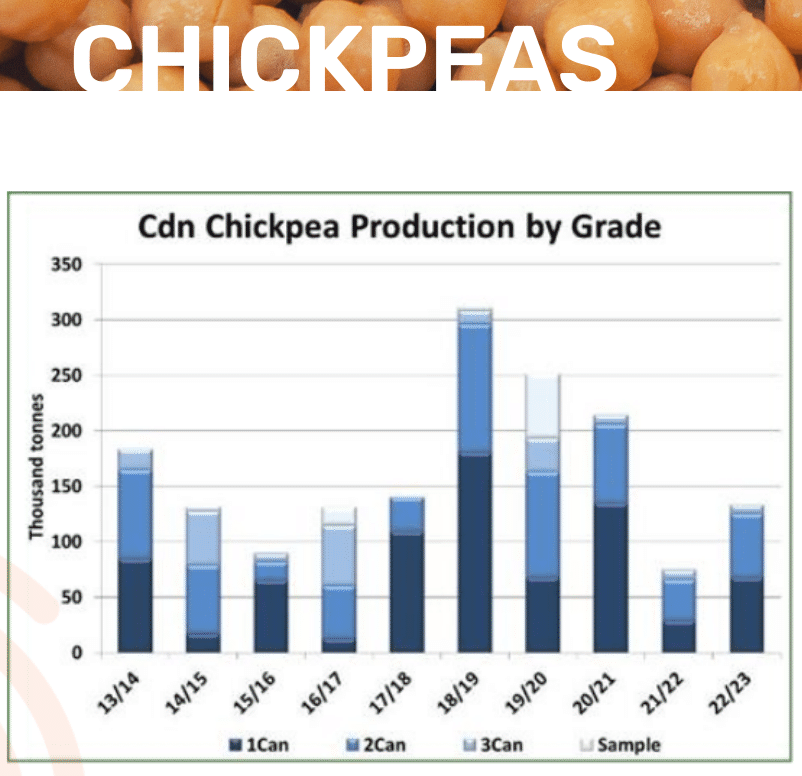

CHICKPEAS

The global outlook for the kabuli chickpea market is generally friendly, although not much of that strength has shown up in the North American market yet. Prices are firming up in markets like India and Mexico where the largest calibre kabulis are traded while markets with 8-10 mm calibres are slower to strengthen.

As the export year progresses and supplies are drawn down, prices are expected to rise. That move will be stronger if farmers are less willing to part with their chickpeas

Black Beans

Peruvian new crop April has pretty much all sold and we expect demand to increase with concerns over Madagascan supply. Verry little if anything expected to come out of USA 2022. Myanmar has harvested and with freight prices easing has become competitive again.

Red Kidney Beans

North American offers still has a defensive tone to the market but a bit more positive with good yields. The harvest finished middle October.

Argentina’s crop has fared better than some of their local counterparts with regards to the impact of the drought, but yields have been low as expected and again quality will be mixed. The best quality will be limited this season and it may be better to buy early to avoid the dregs at the end of the crop.

Butter Beans

US acreage losing out to more profitable crops. China remains expensive particularly with high freight. It may be a good time to consider alternative origins. Peruvian and European options are there if the quality works for your application.