27 May 2026

Supplier Showcase: Italian Tomato Processing with Steriltom & Italtom

Lupa Foods is thrilled to showcase our partnership with Steriltom and Italtom,...

OVERVIEW

It is important to recognise that Durum Wheat Semolina attributes a large portion of overall cost in pasta.

However, in today’s climate, energy has become the key driver of increased costs as opposed to the raw material itself. In 2022, the costing of pasta looks entirely different to previous years, and we need to look past the ingredients list to understand the cost.

Aside from Energy, other contributing factors include:

For Durum wheat, it makes sense for us to focus on two origins: Italy and Canada.

Canada is the leading producer and exporter of Durum wheat semolina, and Italy are key growers, but also are a very important nation for production and usage of the commodity.

Note, some of the information presented is for wheat, not durum wheat. However, these are correlated.

DURUM WHEAT PRICES

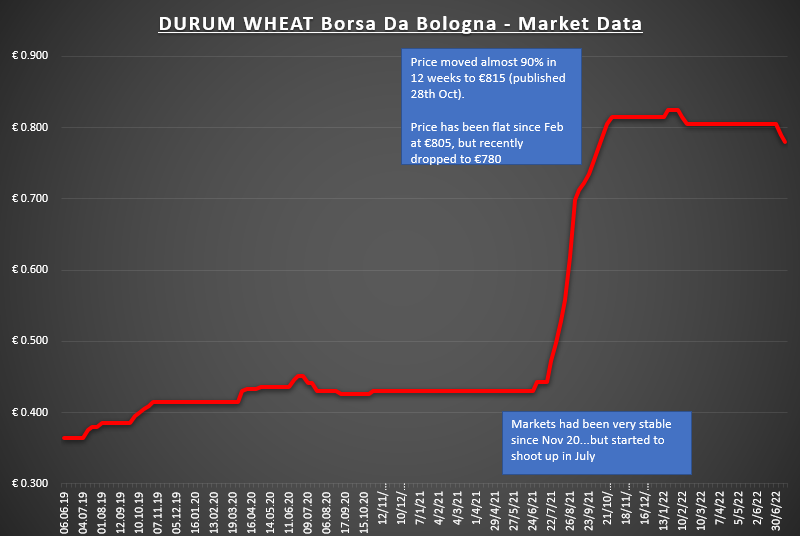

The price of Durum wheat semolina rocketed in August/September of 2021. Since then, the commodity has been fluctuating between £450/£500 PER MT.

As the new harvest is underway/reaching its conclusion, the prices are beginning to decline as stocks are replenished. However, the recent heatwaves in Europe will have an impact towards the upside again.

The other important factor to note is that grain is now being exported again from Ukraine, allowing some relief to demand. We’ve also included Russia, just to demonstrate where their pricing sits.

Notes:

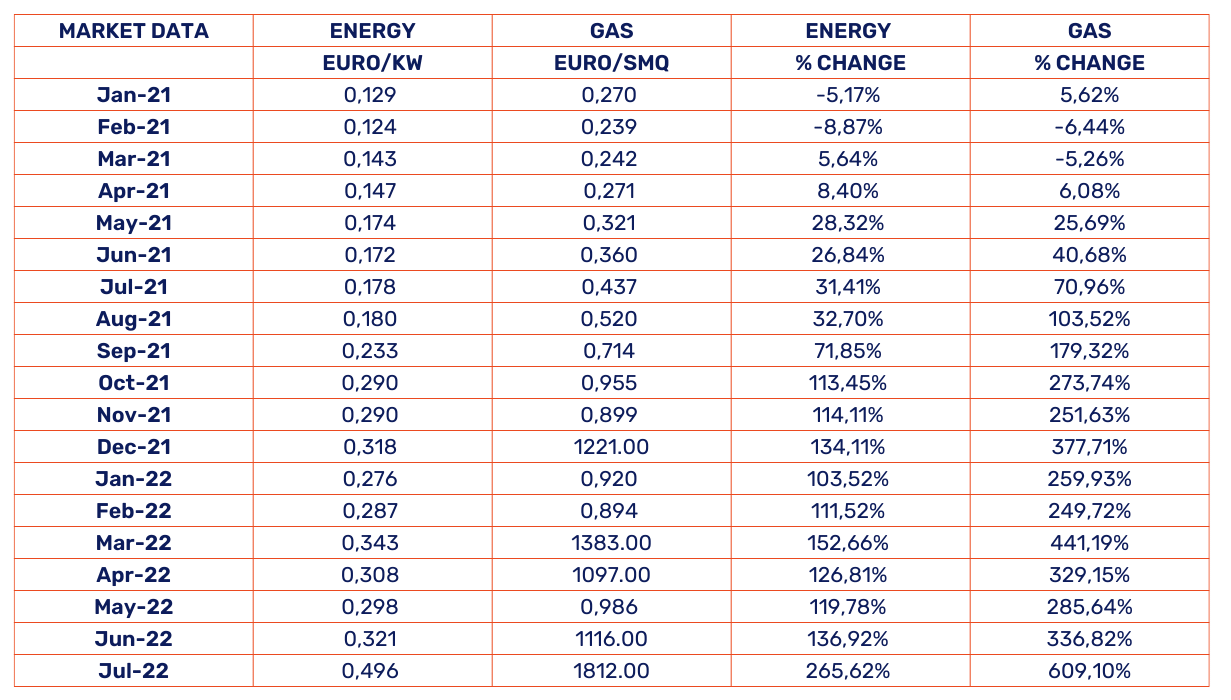

ITALIAN ENERGY AND GAS

Historically energy has made up approximately 4% of the overall cost for pasta production. Due to the recent events in Ukraine and the implications/sanctions connected to Russia, it now represents 17% of the overall cost. This equates to a 304% increase in the energy cost within the cost model.

ITALIAN DURUM WHEAT

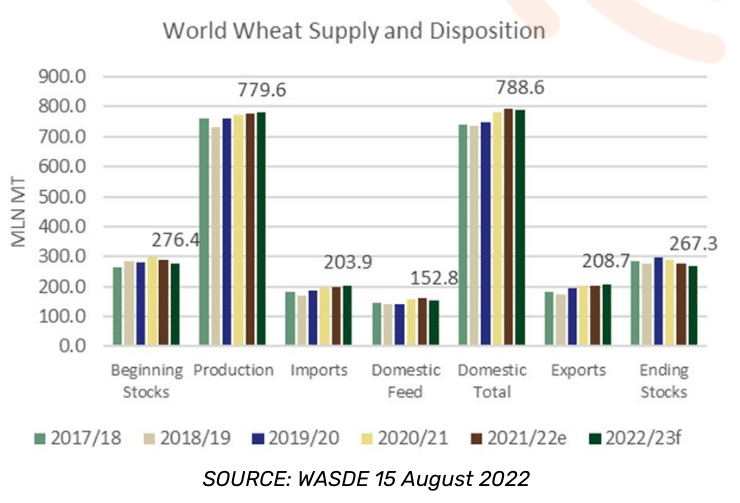

WHEAT OUTLOOK

EU WHEAT OUTLOOK

CANADA WHEAT

Crop conditions for Spring 2022 in Alberta have dropped by 3% in the past 2 weeks to 77% (good to excellent quality), meaning less consumable volume is available.

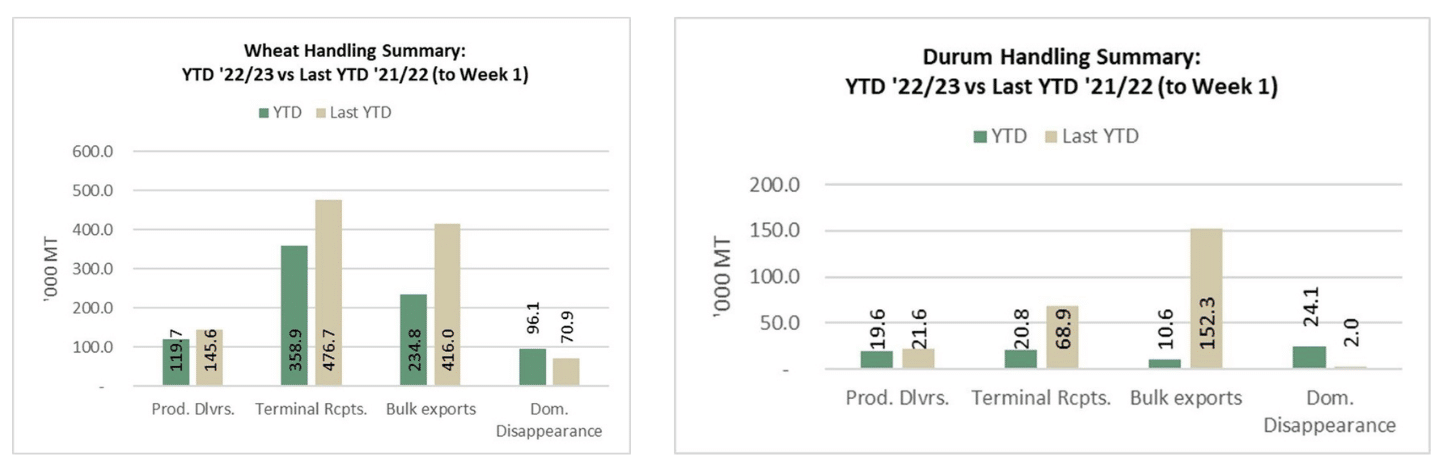

Canada exported 234.8k tonnes of wheat in the first week of shipping season. There are still 1.8m tonnes of old crop supply visible in the supply chain. This will fulfil demand until new crop is available. Large crop in western Canada means that there will be a lot of volume to be transported to manufacturers. This means that there will be pressure on haulage and rail systems to carry grain to its destination. This may inflate operational costs.

Current crop condition is 46% good/excellent, which is down 2% from 2 weeks ago. This is a sign of reduced yield.

Canada exported 10.6k mt of durum in first week of the season. Durum exports are usually low in August/September and pick up in October/November.

SUMMARY